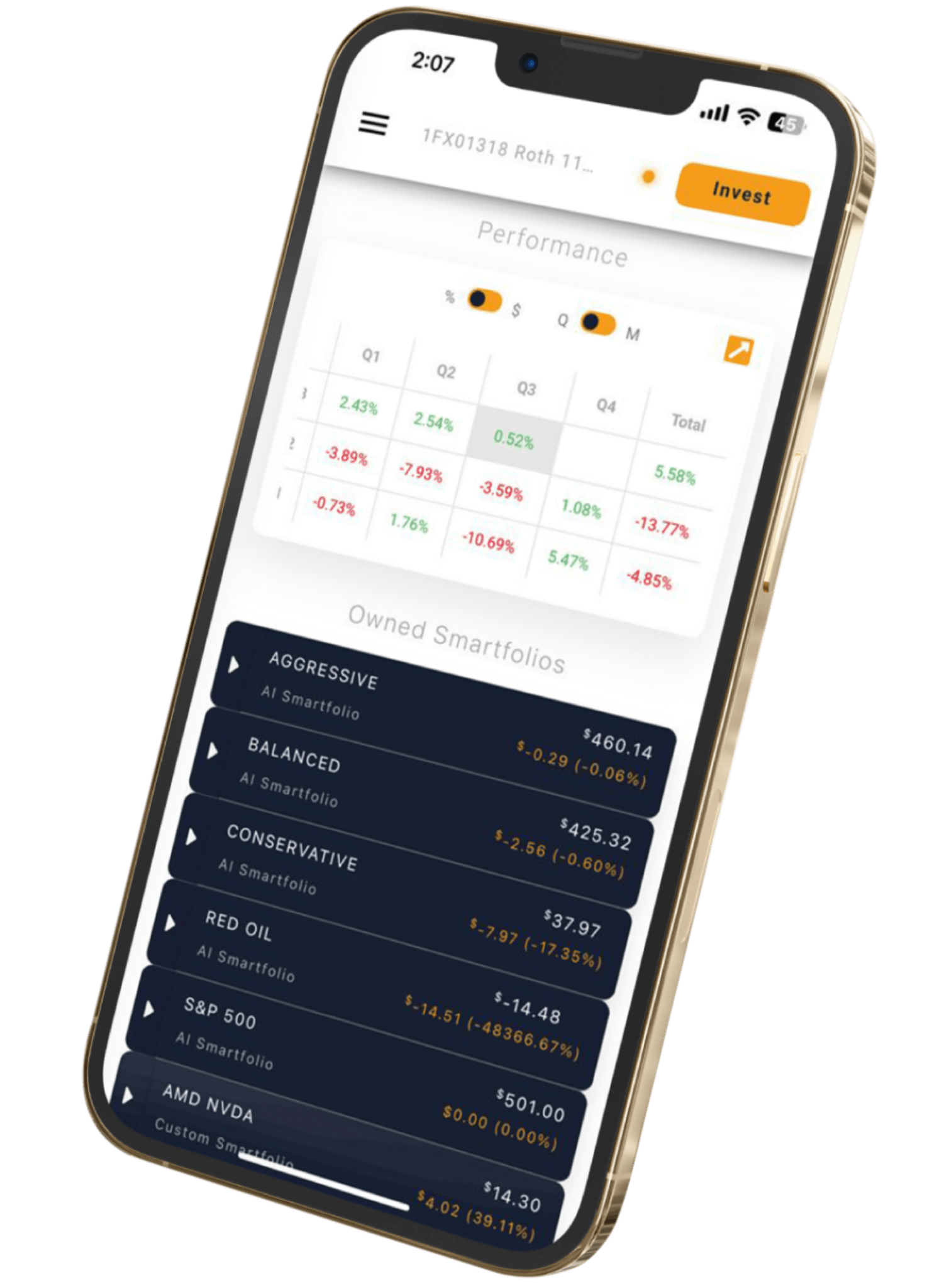

| Wealth Manager | Robo Advisor | Online Broker | ||

|---|---|---|---|---|

| Investments managed with AI | ✓ | ✓ | ||

| Can choose market index strategy | ✓ | ✓ | ✓ | |

| Low minimum investment ($500) | ✓ | ✓ | ||

| Ability to pay 0% in fees | ✓ | ✓ | ||

| Built with protection in mind | ✓ | ✓ | ||

| Intuitive online experience | ✓ | ✓ | ✓ | |

| Choose individual stocks or ETFs | ✓ | ✓ | ✓ |

Real Estate

Private Lending

Syndications

Cryptocurrency

Private Placement

Precious Metals

×

×

Find your payroll provider

Search and select your payroll provider to get started

-

Accupay isolved

Accupay isolved

-

Adams Keegan

Adams Keegan

-

adp run

adp run

-

ADP workforce now

ADP workforce now

-

ADP

-

alcotthr

alcotthr

-

AlphaStaff

AlphaStaff

-

Amplify HR

Amplify HR

-

APS payroll

APS payroll

-

BambooHR

-

BeneCare

BeneCare

-

Bizchecks payroll

Bizchecks payroll

-

bob

bob

-

C2

C2

-

ceridian dayforce

-

click up

click up

-

co advantage

co advantage

-

Coastal payroll

Coastal payroll

-

cognosHR

cognosHR

-

commonwealth payroll and hr

commonwealth payroll and hr

-

CPM Employer services isolved

CPM Employer services isolved

-

creative business resources

creative business resources

-

crescent

crescent

-

deel

-

dominion

dominion

-

employdrive

employdrive

-

empowerhr

empowerhr

-

engage peo

engage peo

-

factorial hr

factorial hr

-

fullstackpeo

fullstackpeo

-

g&a partners

g&a partners

-

GTM

GTM

-

gusto

-

highflyer

highflyer

-

infiniti

infiniti

-

insperity

insperity

-

isolved

isolved

-

justworks

-

keystone

keystone

-

namely

namely

-

netchex

netchex

-

newtek

newtek

-

oasis

oasis

-

obsidianhr

obsidianhr

-

onesource

onesource

-

onpay

onpay

-

oyster

oyster

-

paragon

paragon

-

patriot

-

paychexflex

-

paycom

paycom

-

paycor

-

paydayworkforcesolutions

paydayworkforcesolutions

-

paylocity

-

paynorthwest

paynorthwest

-

payroll network

payroll network

-

payrollofficeofamerica

payrollofficeofamerica

-

payrollontime

payrollontime

-

payrollplushcm

payrollplushcm

-

paytime

paytime

-

payusa

payusa

-

pesonio

pesonio

-

platinum group

platinum group

-

prismhr

prismhr

-

proxushr

proxushr

-

quality payroll

quality payroll

-

questco

questco

-

quickbooksonline

-

remote

-

resourcing edge

resourcing edge

-

rippling

-

sageHR

sageHR

-

sapling

sapling

-

savant HCM evolution

savant HCM evolution

-

sequoiaone

sequoiaone

-

sesame

sesame

-

sheakley

sheakley

-

strategicpayrollsolutions

strategicpayrollsolutions

-

tandemhr

tandemhr

-

the payroll company

the payroll company

-

threadhcm

threadhcm

-

toast

-

TriNet HR Platform (fka Zenefits)

TriNet HR Platform (fka Zenefits)

-

trinet PEO

-

UKG Ready

UKG Ready

-

UltiPro (UKG Pro)

UltiPro (UKG Pro)

-

vensurehr

vensurehr

-

Vfficient

Vfficient

-

wave

-

whirks

whirks

-

workday

-

Xero (international)

Xero (international)